When Bones Speak Louder Than Bank Rules

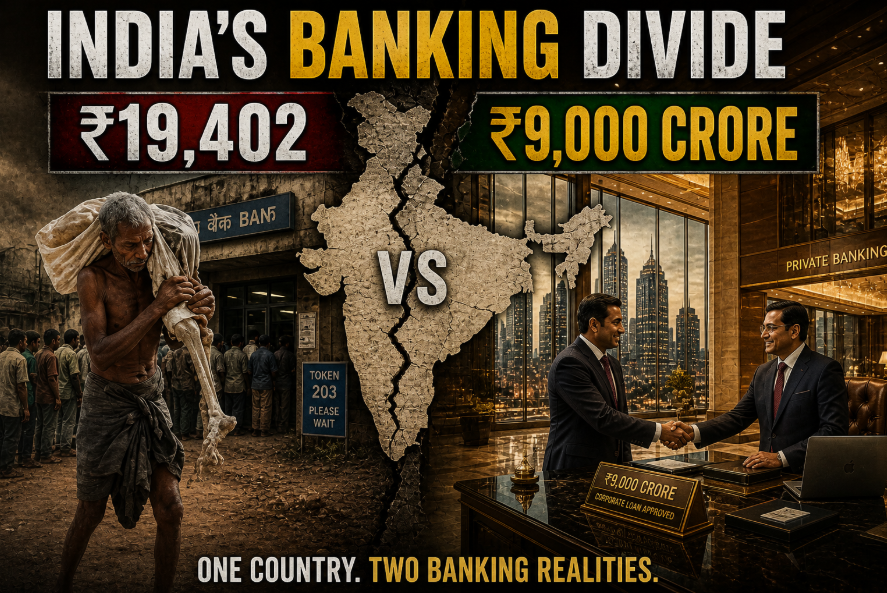

India’s Banking Divide has never stared us more painfully in the face. On April 27th, 2026, Jitu Munda – a 50-year-old tribal man from Dianali village in Keonjhar district, Odisha – walked into Odisha Grameen Bank carrying the skeletal remains of his deceased elder sister, Kalra Munda. He did not carry them as a protest gimmick. Sheer, bone-deep desperation drove him to carry them. His sister passed away on January 26th, 2026, leaving behind a bank account with a balance of just ₹19,402. And yet, for months, the banking system could not find a way to release that money to her legal heirs.

Now, here’s what should make you stop and think. While Jitu sat outside the bank with his sister’s remains, somewhere else in India, a corporate borrower was comfortably defaulting on thousands of crores – and quietly getting his loan restructured. So, let me ask you directly – what does it say about a banking system when a grieving brother must carry a corpse to collect ₹19,402, while a fugitive businessman comfortably writes off ₹9,000 crore from London? That, in essence, is India’s Banking Divide – a chasm so wide, so deep, and so morally staggering that no single statistic can fully capture it. But let me try, anyway. Alarmingly, the numbers, when laid side by side, are staggering – and the stories behind them are even more so. Throughout this blog, I take you through the data, the human cost, the systemic rot, and, finally, the reforms that could actually change things. Buckle up – this is a ride through both the promise and the deep failures of banking in India.

The Keonjhar Case: A Story That Should Never Have Happened

An Incident That Shocked the Nation

Jitu Munda’s sister, Kalra Munda (56), passed away on January 26th, 2026, in Keonjhar district, Odisha. She held a modest account at the Odisha Grameen Bank, Maliposi branch, with a balance of ₹19,402. After her death, Jitu and the other two legal heirs began claiming that amount — a process that any fair and humane system should resolve in days. Instead, it stretched into months of painful bureaucratic back-and-forth. Requests for documentation kept coming in; rural government authorities failed to issue certificates fast enough. Moreover, bank staff mechanically executed protocol, never pausing to consider the human being across the counter. Finally, in a desperate bid to force the bank’s hand, Jitu arrived at the branch carrying his late sister’s remains – and the image went viral, shaking India’s conscience.

The aftermath, at least, moved quickly once the nation was watching. The Indian Overseas Bank, a sponsor of Odisha Grameen Bank, confirmed on April 28–29th, 2026, that after the death certificate and legal heir certificate were finally issued, the bank finally settled the claim of ₹19,402 among the three legal heirs. Physics Wallah founder, Alakh Pandey, announced ₹10 lakh in aid for Jitu Munda. Odisha Chief Minister Mohan Majhi also acknowledged the case publicly. But here is the bitter truth – Public outrage alone forced the settlement. Without the viral photograph and video, Jitu Munda might still be waiting. And that, painfully, is the defining feature of bank rules for death claim in India: the loudly viral wheel gets the grease; the silent poor get nothing. As former RBI Governor Raghuram Rajan once observed: “Financial inclusion is not just about getting a bank account — it is about getting a fair shot at prosperity.” That fair shot was nearly denied to Jitu Munda – over ₹19,402.

India’s Banking Divide: By the Staggering Numbers

₹16.35 Lakh Crore Written Off – And You and I Paid for It

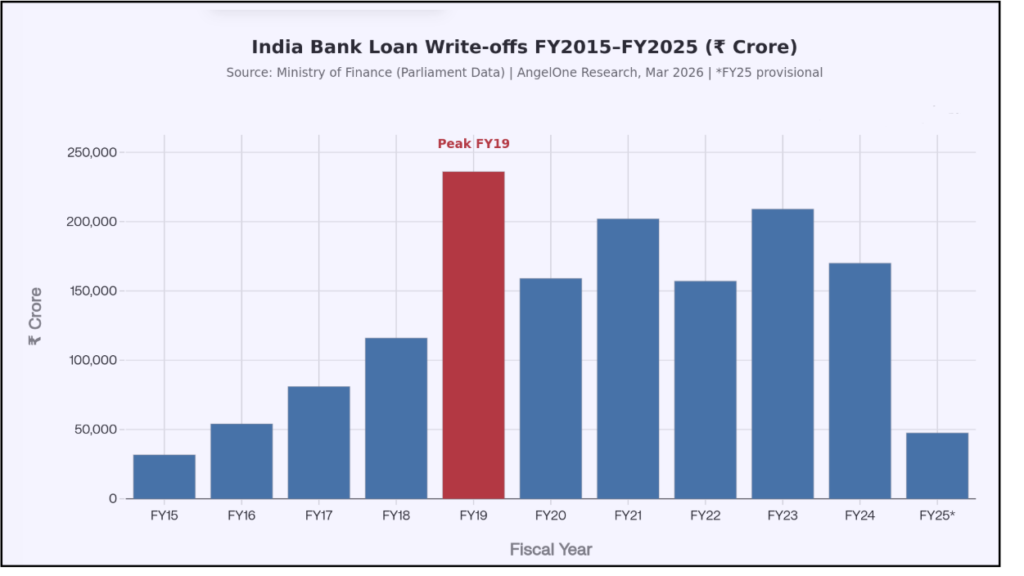

This is where India’s Banking Divide transforms from an emotional story into an economic scandal. Between FY2014-15 and FY2023-24, scheduled commercial banks in India wrote off a colossal ₹16.35 lakh crore in non-performing assets (NPAs) – with banks writing off ₹1.6 lakh crore every single year on average. The highest single-year write-off occurred in FY2018-19, at a jaw-dropping ₹2,36,000 crore. Public Sector Banks drove roughly 60% of these write-offs, with SBI alone writing off ₹1.15 lakh crore between FY2021 and FY2025. Union Bank erased ₹85,000 crore; PNB wiped out ₹81,000 crore; Bank of Baroda shed ₹70,000 crore – all from public balance sheets.

Source: Ministry of Finance (Parliament of India, Lok Sabha/Rajya Sabha Q&A Data); AngelOne Research, March 2026. *FY25 provisional

Now contrast that with ₹19,402 – the amount Jitu Munda’s sister left behind. The annual average write-off (₹1.6 lakh crore) is mathematically unfathomable compared to that sum. Nonetheless, the banking system found it impossible to release that tiny amount without months of documentation. Meanwhile, large corporate borrowers – each with outstanding dues above ₹1,000 crore – remain classified as NPAs, amounting to ₹61,027 crore as of December 2024. Section 45E of the RBI Act legally shields their identities. In other words, loan write-offs in India have quietly become a story of institutional amnesia for the powerful and institutional tyranny for the poor. As former Finance Minister P. Chidambaram pointedly noted: “The debate on waiver or write-off is academic. People who are mighty pleased are Nirav Modi, Mehul Choksi and Vijay Mallya! Rules are made by human beings – and if a rule can be made, it can be unmade too.” That quote cuts straight to the heart of banking inequality in India.

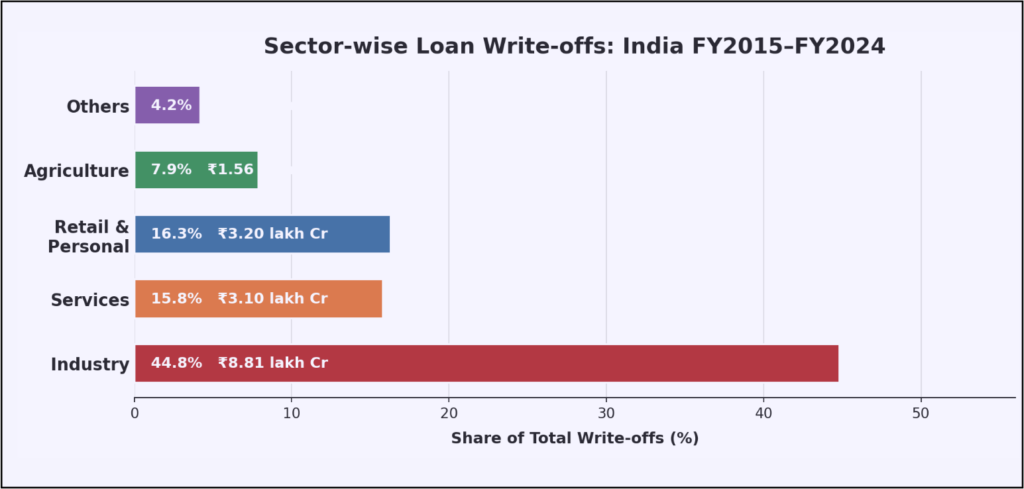

Who Writes Off What – The Sector Story

Large industries alone account for nearly 45% of all NPA write-offs in India over the past decade. The remaining burden is distributed across services, retail, agriculture, and others – but the common thread is clear: the bigger the borrower, the more forgiving the system. Meanwhile, a tribal man in Keonjhar waits months for ₹19,402. The sector breakdown below makes the disparity impossible to ignore.

Source: Parliament of India (Lok Sabha/Rajya Sabha Q&A); TheKanal.in analysis of RBI sector data, 2026

The Contrast: ₹9,000 Crore vs ₹19,402

For the Powerful – Billions, Flexibility, and Freedom

Vijay Mallya – once celebrated as the ‘King of Good Times’ – owes approximately ₹9,000 crore to a consortium of Indian banks and has been comfortably residing in the United Kingdom since 2016. Nirav Modi owed ₹13,000 crore; Mehul Choksi – who orchestrated part of the ₹14,000 crore PNB scam – figures prominently on that same list. Together, just nine fugitive economic offenders carry liabilities of ₹58,000 crore, and banks have failed to recover ₹39,000 crore of that amount. The PNB scam persisted for years because the bank never integrated SWIFT transactions with its core banking platform – a regulatory oversight almost comical in hindsight. These borrowers had access to legal teams, political connections, and international jurisdictions. As a result, banks struggle to recover these amounts over prolonged periods. The contrast with Jitu Munda is not just economic – it is a statement about whose time the banking system considers valuable.

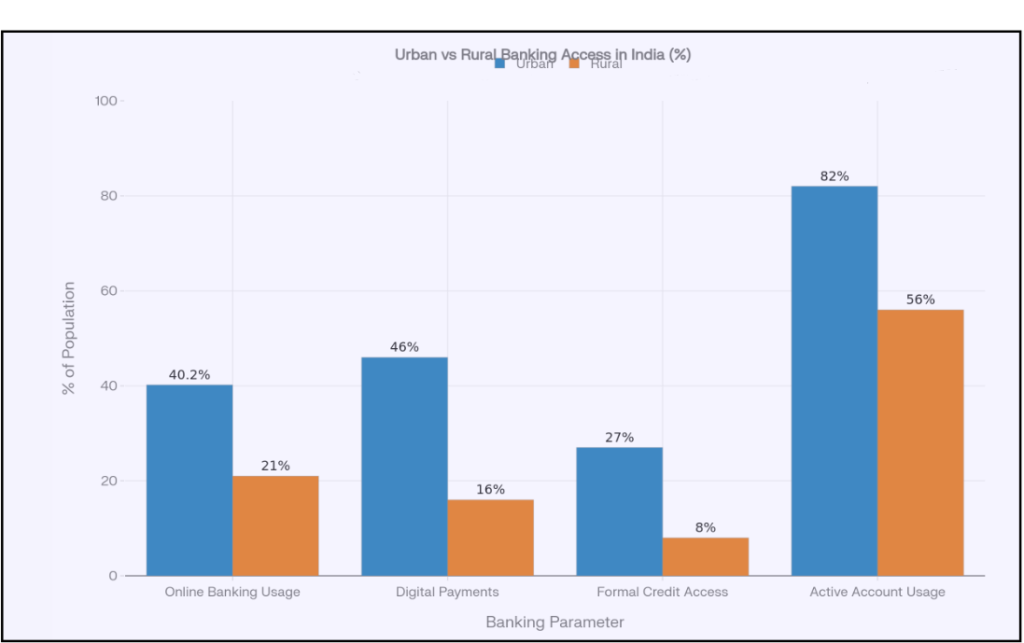

Source: IAMAI India Internet Report 2025; Finextra (Bridging the Urban-Rural Divide, May 2025); NABARD All India Rural Financial Inclusion Survey; India Inclusive Finance Report 2025, ACCESS Development Services

For the Powerless – Documentation, Delays, and Dignity Denied

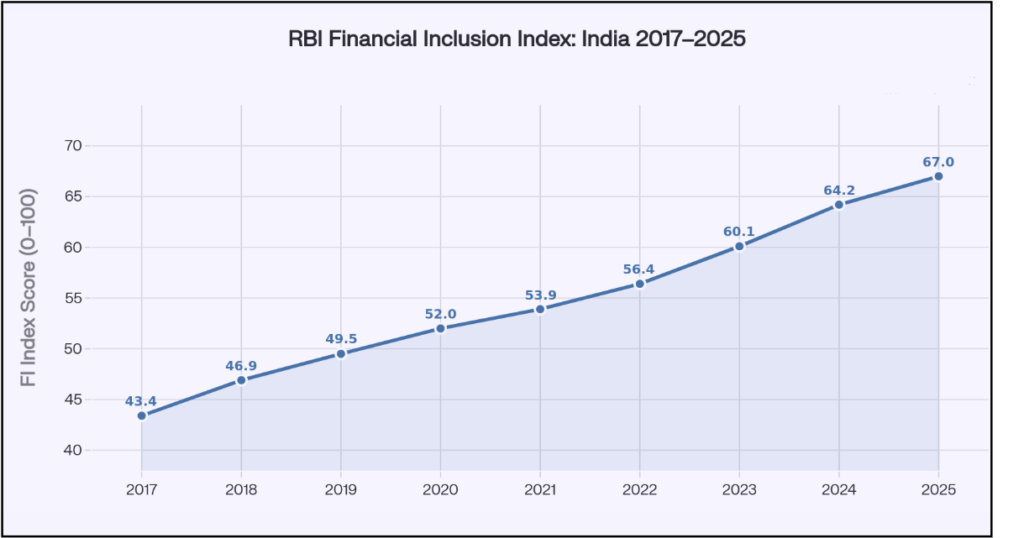

For the powerless, the story is entirely different. Banking inequality in India at its most brutal in rural India – where only 21% of rural residents use online banking compared to 40.2% in urban areas, and where only 16% of rural Indians make digital payments, compared to 46% of urban residents. In Jitu’s case, the system demanded a death certificate and legal heir certificate – documents that take considerable time to procure in rural Odisha, especially for a tribal family with limited access to government offices. Moreover, the RBI’s Financial Inclusion Index stood at 67.0 for March 2025 – a number that sounds impressive until you realise that vast pockets of India’s rural and semi-urban population still remain outside the dignified embrace of the banking system. Private-sector banks, which opened 66% of new branches in FY24, are only now beginning to move into rural areas in a meaningful way. For decades, the rural poor have banked at institutions designed to serve them on paper – but whose internal processes were modelled entirely on urban, educated, documented India.

The Great Indian Banking Inequality Gap – At a Glance

| Parameter | Large Corporate Borrowers | Small/Rural Depositors |

|---|---|---|

| Loan size | ₹100s–₹1,000s of crore | ₹100s–₹10,000s |

| NPA write-offs (decade) | ₹16.35 lakh crore | Not applicable |

| Documentation required | Legal teams available | Death certificate, heir certificate, ID, passbook |

| Resolution speed | Years via DRT/NCLT | Months for ₹19,402 |

| Legal recourse | Full (DRT, NCLT, lawyers) | Virtually none |

| Public identity protection | Yes (Sec. 45E, RBI Act) | No protection |

| Recovery status (fugitives) | ₹39,000 Cr unrecovered | Not applicable |

| Digital access | Full | 21% rural online banking |

Sources: RBI Annual Report, Parliament Data, IndiaToday, ANI

India’s Banking Divide and the Systemic Rot Beneath

Risk Bias, Legal Asymmetry, and Administrative Cowardice

Banking inequality in India does not exist by accident – it is baked into the architecture of the system. Frontline bank staff at rural branches often follow rules mechanically to protect themselves from accountability. Incidentally, this creates a culture of rigid compliance that inflicts its greatest human damage at the lowest transaction values. On the other hand, large borrowers navigate the same system with armies of chartered accountants, lawyers, and relationship managers who know exactly which levers to pull. As former RBI Governor, Shaktikanta Das, said at the Economic Times Financial Inclusion Summit: “India has come a long way in facilitating access to banking services, but the quality of access – and the dignity of that access – must be our next frontier.” The Keonjhar case precisely exposed that dignity gap. Moreover, the IDFC First Bank ₹590 crore fraud (2026), where the Haryana government accounts showed unexplained discrepancies, again highlights how fraud detection remains far more active for large accounts than for small ones.

Deep and wide structural fault lines define this broken system. First, there is risk perception bias: banks treat small customers with suspicion – demanding exhaustive proof for withdrawals of ₹19,402 – while extending hundreds of crores to corporations based on projected cash flows and relationship capital. Second, there is legal asymmetry: a corporate defaulter can tie recovery proceedings in Debt Recovery Tribunal (DRT) or National Company Law Tribunal (NCLT) for years, while a rural widow cannot afford to even write a legal letter. Third, and most insidiously, there is administrative inflexibility: banks bend, waive, and ‘restructure’ the same rule book for powerful borrowers – yet slam it shut as an immovable stone wall against the vulnerable. The result – as the Keonjhar incident proves beyond any doubt – is a banking system where bank rules for death claims in India become instruments of humiliation rather than protection.

Similar Incidents: Keonjhar Was Not the First Cry

India’s Long History of Bureaucratic Cruelty in Banking

Tragically, the Keonjhar case is not an isolated aberration – it is the most visible tip of a very large and cold iceberg. Across India, pensioners are routinely required to submit “life certificates” – physically appearing at bank branches to prove they are still alive – a process so humiliating that several elderly pensioners have reportedly collapsed during the exercise. Banks have forced farmers in rural Maharashtra and Vidarbha to endure long delays in accessing Kisan Credit Card funds, with documentation barriers that mirror exactly what Jitu Munda faced. In Rajasthan and Uttar Pradesh, banks have turned away widows seeking their husbands’ Jan Dhan account balances for months on end. Meanwhile, at the other end of the spectrum, the Yes Bank crisis of 2020 saw retail depositors lose immediate access to their own money – not because they defaulted, but because the bank’s own promoters had indulged in reckless lending to troubled corporate groups.

The government launched Jan Dhan Yojana in 2014, opening over 53 crore accounts by 2025 — a genuine, well-intentioned achievement in financial access. However, as the RBI’s own Financial Inclusion Index of 67.0 indicates, access is not the same as equitable service. Regional Rural Banks – designed specifically for rural financial inclusion – have opened approximately 9–10 crore accounts, representing 16–19% of total PMJDY beneficiaries, but critical gaps in digital infrastructure continue to cripple their outreach. The UPI revolution, with 16.99 billion transactions in January 2025 alone, has transformed urban and semi-urban India – but only 16% of rural populations engage in digital payments. Inclusion requires not just an open account – it requires an open, welcoming, and dignified door every single time.

RBI Guidelines: What the Rules Actually Say

The Framework That Exists – and the Gap Between Paper and Practice

The RBI has, to its credit, issued detailed guidelines on settling deceased depositors’ accounts. For accounts with balances up to ₹5 lakh, simplified nomination-based settlement is allowed without requiring succession certificates or letters of administration. For accounts below ₹50,000 with no nominee, a simple indemnity bond and a declaration from the claimant should suffice. The RBI explicitly instructs banks to be ‘sympathetic and helpful’ and to settle claims within 15 days of document submission. Moreover, under bank rules for death claims in India, the Master Circular on Customer Service mandates that frontline staff actively assist claimants in identifying the minimum documentation they need. In theory, therefore, the system Jitu Munda encountered was not supposed to exist. In practice, it exists everywhere – because the gap between RBI guidelines and ground-level bank behaviour is a chasm that no circular alone can close.

Source: Reserve Bank of India Annual Report; PIB Press Release – “67 and Rising: India’s Financial Inclusion Gains Momentum,” August 2025

The Finance Ministry has clarified that NPA write-offs are not waivers – banks continue pursuing recovery through DRTs, Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act proceedings, and NCLT insolvency mechanisms. Scheduled commercial banks drove Gross NPAs down to 2.3% in FY25 – a 13-year low – through improved provisioning and governance. The government’s point is well-taken – the system is technically improving at the macro level. But “technically improving” means very little to a man sitting outside a branch with his sister’s remains. The RBI’s FI-Index of 67.0 must climb relentlessly toward 100 – and that climb demands not just branch openings, but a cultural transformation within banking institutions toward human-centred, compassionate service. Loan write-offs in India must carry as much transparency and public accountability as every small claim denial.

The Human Cost: Dignity Is Non-Negotiable

When Rules Stop Being Safeguards and Become Punishments

Let me be direct here – there is no sanitised way to discuss what happened in Keonjhar. A man carried his dead sister to a bank because he had no other option. That is not a story about documentation. That is a story about a system that has completely lost its moral compass in its dealings with the poor. In rural and semi-urban India, death certificates can take weeks or months to issue. Family members may not understand formal banking procedures. Local branch staff may lack adequate guidance to help claimants navigate the process. And the banking inequality in India that results from all of this is not just economic – it is existential. The system strips people of their dignity at a moment of maximum vulnerability. The human cost of this systemic failure – in stress, in lost wages, in psychological trauma, in erosion of institutional trust – is immeasurable and largely invisible.

Furthermore, the asymmetry extends well beyond death claims. India’s pensioners face the annual indignity of “life certificate” submissions. Banks effectively exclude PMJDY account holders in tribal belts through dormant account penalties and zero-balance pressures. Farmers with Kisan Credit Cards face renewal delays that can destroy an entire crop cycle. And at the other end of the spectrum, while all of this happens daily, loan write-offs in India continues at a pace of ₹1.6 lakh crore annually – with the identities of the largest defaulters shielded by law. The moral inversion is total: the poor must prove everything, endlessly, while the powerful are trusted – and then protected – by default. As the EAC-PM’s 2026 paper on Financial Inclusion states: “Financial inclusion represents a fundamental human rights imperative, linking economic access to dignity and opportunity.” Jitu Munda’s journey to that bank was a desperate plea for exactly that. Zero discrimination should exist in a system that serves all.

What Must Change: Reforms for a Truly Inclusive System

Structural Fixes That Go Beyond Slogans

India has the architecture for change – but the will to implement it at granular level remains stubbornly inconsistent. First, simplified claim processes for small amounts (below ₹1 lakh) must be mandated with hard timelines – 7 working days maximum, with a single-window interface at every rural branch, eliminating the need for multiple visits to multiple offices. Second, human-centred training for bank frontline staff must be institutionalised – regular sensitisation workshops, performance metrics that include customer satisfaction scores, and a grievance escalation mechanism that every branch displays visibly and keeps readily accessible. Third, faster rural documentation systems – particularly for death and legal heir certificates in tribal and remote areas – require inter-departmental coordination between banking regulators and state governments. Fourth, mandatory transparency in NPA resolution: Banks must publicly disclose every corporate write-off or restructuring, along with a clear recovery timeline. The current asymmetry – small claimants grilled while large defaulters are shielded – is legally dubious and morally bankrupt.

Fifth, and critically, India must invest heavily in digital literacy in rural areas, where only 21% of residents currently use online banking, ensuring the UPI revolution genuinely reaches the last mile. Authorities must apply the Fugitive Economic Offenders Act (2018) and the SARFAESI Act urgently and consistently against large defaulters – not invoke them selectively. Regulators must hold private-sector banks – which opened 66% of new branches in FY24, with 44% in rural and semi-urban areas – to the same service standards as public sector banks for vulnerable depositors. Bank rules for death claims in India must be rewritten to be compassionate by design, not merely compliant by default. And perhaps most importantly, every bank – rural or urban, public or private – must move beyond “following protocol” to asking the harder question: does this protocol serve the human being sitting in front of me?

Inclusion Is a Moral Imperative, Not a Metric

From Personal Change to National Transformation

India’s Banking Divide will not close through government circulars alone. It will close when each of us – as citizens, account holders, voters, and human beings – demands that the banking system treats every person with equal dignity regardless of the size of their account. On a personal level, that means staying informed about your banking rights, using the RBI Integrated Ombudsman Scheme (cms.rbi.org.in) whenever your rights are violated, filing RTI requests when institutions are unresponsive, and actively helping financially vulnerable people in your community navigate the banking system. If you know someone in a rural area struggling with a deceased family member’s claim, guide them directly to the RBI’s Master Circular on Customer Service – that document exists precisely for situations like Jitu Munda’s. Awareness demands action – it serves as the first act of accountability.

On a social and national level, addressing India’s Banking Divide means holding corporate defaulters and the institutions that enabled them publicly accountable – through journalism, through voting, through activism, and through civic discourse. It means demanding that banks and regulators publicly account for every rupee of the ₹16.35 lakh crore written off over a decade – not merely record it as an accounting entry. It means insisting that we treat the Financial Inclusion Index of 67.0 as a starting point, not a trophy. Further, it means every Jitu Munda who walks into a bank carries within him not just grief — but a mirror that shows us exactly what kind of nation we are building. Banking inequality in India is ultimately a symptom of a deeper disease: a system where rules are negotiable for those with power and immovable for those without. The cure demands no complexity – just empathy, accountability, transparency, and the political will to treat every citizen as equally deserving of financial dignity. That is the India we must build – one account, one claim, one dignified interaction at a time.

At ExpressIndia.info, we believe that a nation’s true financial integrity is not measured by how generously it forgives its most powerful borrowers – but by how swiftly and humanely it serves its most vulnerable ones. If this blog resonated with you, share it widely – because awareness is the first step toward accountability. Report any banking injustice to the RBI Integrated Ombudsman at cms.rbi.org.in. And comment below with your story – because every voice matters in closing India’s Banking Divide.

#IndiasBankingDivide #BankingInequalityIndia #FinancialInclusionIndia #NPAWriteOffs #JituMunda