Why this war suddenly feels very close

The impact of Israel-Iran war on India is no longer a matter of distant speculation. The war is already more than a month old, with no clear signs for a ceasefire in sight yet. Consequently, it has turned into a live stress test for the Indian economy, the rupee, and the livelihoods of millions. Oil prices have spiked, gas supplies have been disrupted, and financial markets have become more volatile, all within a matter of weeks. India finds itself particularly exposed because it imports close to 90 percent of its crude oil. Moreover, it depends heavily on the Middle East for gas, LPG and fertilisers, as well as for a very large share of its remittances. In that sense, this conflict is less a foreign‑policy essay topic and more a pressure gauge on India’s external vulnerability. Former NSA Shivshankar Menon’s warning that “no region impinges on India’s security as immediately as West Asia” now reads less like analysis and more like a weather report. The immediate question, therefore, is not whether the war affects India, but how severely, how quickly and for how long.

At the same time, it is important to separate the emotional noise from the measurable impact. Policymakers, markets and households are all trying to understand two things: first, the immediate, quantifiable damage already visible in prices, growth forecasts and remittance risks; and second, the short, medium and long‑term implications if the Strait of Hormuz remains effectively weaponised. In this context, Gita Gopinath’s remark that even an “average” oil price of 85–100 dollars this year could shave off up to one percentage point from India’s growth captures the stakes in concrete terms. The rest of this blog will map those stakes systematically: what is happening now, what could happen if the war drags on, and what India must do to protect both its macro stability and its people.

Impact of Israel-Iran War on India: Immediate Economic Shock

Right now, the impact of Israel-Iran War on India shows up most starkly in energy prices and growth expectations. Brent crude has climbed from around 80 dollars to well above 120 dollars per barrel since the conflict escalated. Besides, some scenarios now openly discuss the risk of 150–200 dollars if the Strait of Hormuz remains effectively closed for longer. Liquefied natural gas prices have nearly doubled after the attack on Qatar’s Ras Laffan facility and subsequent force majeure declarations, which has tightened LNG availability worldwide. India gets roughly 40 percent of its LNG imports from Qatar and about half of its crude and more than three‑fourths of its LPG imports through the Hormuz route. Due to the present imbroglio, it has resulted in shortages of supplies of these vital resources. As a direct result, the rupee has weakened, bond yields have firmed up, and financial markets are more volatile than they were at the start of the year. Although these shifts are not yet a full‑blown crisis, they clearly represent a significant external shock that could intensify if conditions deteriorate.

Growth forecasts capture the scale of that shock in numbers. Goldman Sachs has cut its India growth projection for calendar year 2026 from about 7 percent to 5.9 percent, explicitly citing higher oil prices, a weaker rupee and energy supply risks as key reasons. Gita Gopinath has indicated that if oil averages around 85 dollars, India might lose roughly half a percentage point of growth relative to earlier expectations, and if it stays nearer 100 dollars, the loss could approach one full percentage point. Reuters analysis suggests that the Israel-Iran war will likely weigh more on Indian growth than on inflation, keeping interest rates lower for now but squeezing growth space nevertheless. In other words, the immediate impact of Israel-Iran War on India is a clear downgrade in growth prospects, from a comfortable 7‑plus narrative to something closer to the mid‑5s or low‑6s. The headline story is therefore not one of a collapse, but a slower and more constrained recovery path.

Energy prices, inflation and India’s Middle East energy dependence

Due to India’s high Middle East energy dependence, energy shocks quickly become inflation concerns. India imports close to 90 percent of its crude oil needs, with roughly half coming from West Asia, and depends heavily on Middle Eastern suppliers for LNG and LPG as well. When oil prices rise by 50 percent in a short window, as they have during this conflict, models used by Indian policymakers suggest that inflation could rise by 50–100 basis points if the shock is fully passed through. So far, state‑owned oil companies have partially absorbed the blow by compressing their marketing margins, which has kept pump prices from rising as much as global benchmarks. However, that strategy creates its own pressures on corporate balance sheets and may not be sustainable if prices remain elevated for many months.

Inflation pressures are already visible in input costs across several sectors. Higher gas and fuel prices are pushing up costs in power generation, fertilisers, cement, steel, chemicals, aviation and logistics. If those costs are increasingly passed on, consumers will face higher electricity tariffs, costlier air travel, and more expensive goods transported over long distances. At the same time, the rupee’s depreciation against the dollar – estimates suggest a 4–5 percent slide this year alone – adds an additional layer of imported inflation, because many commodities are priced in dollars. In that sense, the impact of Israel-Iran War on India is working through a double channel: more expensive energy and a weaker currency, both of which lean in the direction of higher domestic prices. The Reserve Bank so far expects inflation to remain within its target band, but much closer to the upper end than previously hoped.

Sectoral stress: Gas shortages, Industry margins and Household budgets

One of the clearest short‑term effects has been on gas‑dependent sectors. The strike on Ras Laffan and disruptions in Qatari LNG shipments have created tighter gas availability and higher spot prices, which directly affect Indian buyers with long‑term contracts and those dependent on spot cargoes. Gas‑based power plants, city gas distributors and industrial users in sectors such as ceramics, glass, fertilisers and some chemicals are feeling this pinch first. This is because they cannot easily switch to other fuels without losing efficiency and facing new investment costs. Reports of curtailed gas allocations, renegotiated contracts and prioritisation of essential uses are early signs of stress along this channel.

Households are seeing the impact in more familiar ways. LPG refill prices have moved up, and there are concerns about rationing or delays in some pockets, especially where supply chains were already stretched. Restaurants, small eateries and bakeries – which rely heavily on commercial LPG and CNG – are facing sharp increases in input costs, forcing them to raise menu prices, reduce portions, scale back hours, or temporarily close marginal outlets. More broadly, higher logistics costs are feeding into the prices of staples, fresh produce and everyday consumer goods, albeit gradually rather than in one dramatic leap. For many urban families, the impact of Israel-Iran War on India is therefore showing up as a set of small but persistent increases: slightly higher cylinder bills, slightly costlier meals, slightly steeper cab fares. Over six to twelve months, these “small” increases could accumulate into a noticeable squeeze on real disposable income.

Impact on the Indian economy: Growth, Rupee and Markets

From a macro‑financial perspective, the Israel-Iran conflict impact on the Indian economy is traversing through growth, the rupee and financial markets. As mentioned earlier, growth projections for 2026 have already been reduced by major forecasters, and a few have suggested that the combined oil and remittance shock could cumulatively shave off up to one percentage point of GDP over the next year or two if conditions remain adverse. Meanwhile, the rupee has weakened as higher energy imports widen the trade deficit and as investors demand a higher risk premium for emerging markets during periods of global uncertainty. Bond yields have drifted upward, reflecting concerns about a larger current account deficit and potential fiscal stress if the government expands subsidies or defers fuel‑tax adjustments.

Equity markets have oscillated with the news cycle, selling off when missile attacks or shipping incidents dominate the headlines, and stabilising when diplomacy appears to be making progress. Banks, energy companies, aviation stocks and some consumer‑facing sectors have been particularly sensitive to these swings. In this environment, the impact of the Israel-Iran conflict on the Indian economy is less about a sudden crash and more about a general tightening of financial conditions: costlier capital, greater earnings uncertainty and more cautious corporate investment plans. For ordinary investors and savers, that translates into higher volatility and a stronger link between global news flow and domestic portfolio values. For policymakers, it complicates the already delicate task of supporting growth while keeping inflation and external balances under control.

India’s Gulf remittances risk and the Indian diaspora

India’s Gulf remittances risk is another crucial dimension of the impact of Israel-Iran War on India. India received around 135–138 billion dollars in remittances in FY25, with roughly 38 percent – about 50 billion dollars – coming from Gulf countries such as the UAE, Saudi Arabia, Qatar, Kuwait and Oman. These inflows have financed roughly 40–42 percent of India’s merchandise trade deficit in recent years, acting as a stabilising force for the balance of payments. If geopolitical risks or economic slowdown in the Gulf lead to a 10–20 percent decline in remittances, economists estimate that India could lose 5–10 billion dollars a year in foreign‑exchange receipts. That gap would need to be filled either by higher borrowing, more volatile capital inflows, or a smaller cushion for the current account deficit.

So far, the visible change is more psychological than numerical. NRIs in Gulf countries are understandably more anxious about job security, contract renewals, and the safety of their families. Some professionals in sectors like aviation, logistics, hospitality and construction have already returned to India or accepted offers in other geographies, while others are adopting a wait‑and‑see approach. States such as Kerala, Maharashtra, Tamil Nadu, Telangana and Karnataka – which together receive nearly two‑thirds of India’s remittances – are closely watching these developments. Over the next twelve to twenty‑four months, India’s Gulf remittances risk could become more concrete if the conflict leads to sustained project delays, cost‑cutting or slower hiring in Gulf economies. For many families, this would mean adjusting consumption plans, postponing investments, or rethinking education and migration strategies.

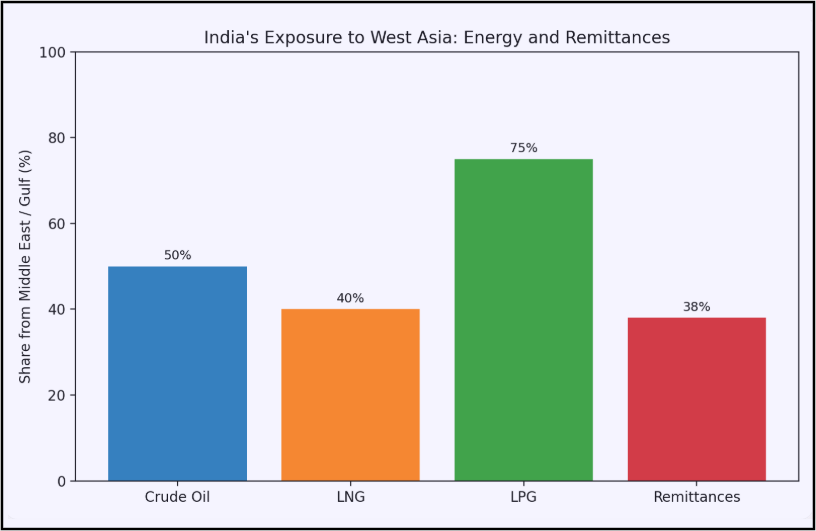

India’s exposure to West Asia

| Indicator | Approximate picture |

|---|---|

| Crude oil import dependence | Around 85–90% of crude is imported |

| Share of crude from Middle East | Roughly half of total crude imports |

| LNG imports from Qatar | Around 40% of India’s LNG imports |

| LPG imports via Strait of Hormuz | More than three‑fourths of LPG imports |

| Annual remittances to India (FY25) | About 135–138 billion USD |

| Share of remittances from Gulf countries | Roughly 38% (≈50–51 billion USD) |

Source: Aggregated from recent Indian energy statistics, RBI and World Bank remittance data, and mainstream economic reporting on India–Gulf linkages

Short‑term outlook (next 6–12 months): Likely scenarios for India

Based on current information, the most relevant horizon of interest is the next six to twelve months. In that period, the impact of Israel-Iran War on India will largely depend on the evolution of three variables: average oil prices, LNG availability from Qatar and other suppliers, and the stability of remittance flows from the Gulf. If Brent averages around 90–100 dollars and LNG markets remain tight but manageable, growth may slow but remain respectable, and inflation could stay within the upper half of the RBI’s target band. If prices rise significantly above that band or if gas disruptions worsen, the pressure on growth and on household budgets will correspondingly intensify.

At the same time, policy choices will matter. If the government continues to shield consumers through suppressed fuel taxes or company margins, inflation may appear better‑behaved, but corporate balance sheets and fiscal metrics will feel the stress. If it allows more of the global price signal to pass through, households and small businesses will bear a larger share of the immediate pain. Either way, the impact of the Israel-Iran conflict on the Indian economy will likely manifest as a period of somewhat slower growth, higher prices, and more cautious sentiment across sectors that depend heavily on energy and external demand. For families, farmers, urban workers and NRIs, this translates into a year where careful budgeting, job stability and resilience matter more than chasing big, risky opportunities.

Three short‑term scenarios for Israel-Iran conflict impact on the Indian economy

| Scenario | Oil / gas pattern | Likely impact on India (0–12 months) |

|---|---|---|

| Contained escalation | Prices elevated but stable | Growth 6–6.5%; inflation near upper band |

| Prolonged disruption | Sustained high prices | Growth 5.5–6%; higher inflation; rupee weaker |

| Severe regional spillover | Sharp, long‑lasting surge | Growth <5.5%; high inflation; fiscal stress |

Source: Synthesised from recent forecasts and scenario analysis by Goldman Sachs, IMF commentary, Reuters and other mainstream macroeconomic assessments.

Medium‑term risks (2–3 years): what if tensions persist?

Although this blog focuses mainly on the present and near future impact, it is useful to briefly outline what could happen over a two to three-year horizon if the war remains unresolved and if the Strait of Hormuz continues to be periodically weaponised. In such a scenario, the impact of Israel-Iran War on India would likely become more structural: chronic energy price volatility, recurring gas and fertiliser supply worries, and a persistent risk premium in the rupee and bond markets. Growth could average lower than India’s potential, not because of domestic demand weaknesses alone, but because external shocks keep forcing bouts of monetary and fiscal tightening.

Furthermore, if India’s Middle East energy dependence remains high, each new flare‑up could reset the cycle: oil spikes, rupee weakens, remittances wobble, inflation resurfaces, and inequality widens as poorer households struggle to cope. However, this medium‑term risk picture also points to a path of opportunity: a strong case for accelerating renewables, domestic gas production where feasible, storage, electric mobility and energy efficiency, as well as for diversifying trade and remittance linkages beyond a single region. In that sense, the same conflict that exposes vulnerabilities can also provide political and analytical momentum for change – if India chooses to treat it as a structural challenge rather than just another severe but temporary shock.

Safeguarding India’s interests: Practical precautions and priorities

Given the evolving situation, what precautions should India take to protect its economic and social interests? On the energy side, experts consistently highlight three priorities. First, deepen diversification of crude and gas sources, including from Russia, the Americas and Africa, to lower exposure to any one chokepoint like Hormuz, even if logistics costs marginally increase. Second, accelerate the expansion of strategic petroleum reserves and consider buffer stocks for critical fertiliser inputs, so that temporary disruptions or price spikes do not immediately translate into domestic shortages. Third, push harder on the structural agenda: more renewables, better grids, energy‑efficient buildings, electric public transport, industrial efficiency, and mostly importantly energy conservation, which together reduce India’s Middle East energy dependence over time.

On the macro‑social side, targeted protection for the most vulnerable groups will matter more than broad, blunt measures. This could include time‑bound support for low‑income households facing LPG and food‑price shocks, smart use of direct benefit transfers, and careful calibration of fuel taxes so that better‑off consumers still see some price signal. For Gulf‑exposed states, India’s Gulf remittances risk suggests the need for contingency plans: skilling programmes for potential returnees, local employment schemes, and credit access for small businesses that rely on remittance‑driven demand. From a diplomatic perspective, continued engagement with all major actors in West Asia to keep shipping routes open and to safeguard Indian workers remains essential, but it should occur without assigning blame or taking sides in the conflict itself. Overall, the impact of Israel-Iran War on India can be managed, but not ignored, and it calls for a blend of near‑term cushioning and long‑term re‑design rather than either panic or complacency.

In that sense, the war is both a test and an opportunity. It is a test of how well India can handle externally driven shocks without losing its growth momentum or leaving its most vulnerable citizens exposed. It is also an opportunity to align energy policy, external strategy and social protection more closely with the realities of a world where regional conflicts can quickly spill across borders through prices, trade and people. At ExpressIndia.info, we will continue tracking how this fast‑moving conflict shapes India’s economy and society, translating complex global events into clear, people‑centred insights for our readers.

#IsraelIranWar #ImpactOnIndia #IndiaEconomy #EnergySecurity #GulfRemittances

Why India gets affected?

It is because of India’s skewed foreign policy.

We have deviated from our policy of nonalignment post 2014.

We do have expert economists, external affairs, militia etc.

But our governmental leadership lacks proper education and diplomacy. The leadership is all the time engaged in internal politics of religion, language, caste etc.

So even the educated experts toe the line of governmental authority for fear of repercussions or for gaining selfish gains.

Moreover, the watch dog called the media are totally surrendered because either they are bought or threatened to submission.

The Iran crisis is no longer just an oil issue but a wider global supply-chain risk. India remains heavily dependent on Gulf crude, so any prolonged disruption will immediately impact fuel prices, inflation, and transport costs. The crisis is also affecting helium supplies, which are essential for semiconductor manufacturing, electronics, and critical medical equipment. At the same time, fertilizer supplies moving through the Gulf are under severe stress, posing a direct threat to agriculture and food production worldwide. The longer the crisis continues, the greater the shortage of fertilizers during key planting seasons, which can sharply reduce crop yields. This significantly increases the risk of a global food crisis and even famine in the most vulnerable regions. If the conflict drags on, it could evolve into a combined energy, electronics, and food-security emergency with serious consequences for India and the world.

You’ve summed it up very well – this has clearly moved from a pure oil shock to a broader supply‑chain crisis touching energy, fertilisers, and even helium for chips and medical uses. For India, the immediate stress is on fuel, fertiliser and freight costs, with knock‑on risks for farmers, food prices and growth if Gulf routes stay disrupted into key sowing seasons. That said, India does have some buffers – diversified suppliers, strategic reserves and the ability to prioritise critical sectors – so the challenge now is using those cushions wisely while accelerating longer‑term fixes in energy security, fertiliser sourcing and supply‑chain resilience.